Carbon Free Future

The UK's most ambitious clean energy programme: 28 coastal mega-sites across all four nations delivering total energy independence by 2055. The Pathfinder Programme proves the technology with 6 single-SMR sites by 2033 — then scales modularly to transform the United Kingdom into an Energy Superpower.

What is Carbon Free Future?

Imagine a United Kingdom where your heating is free, your energy is home-made, the NHS gets free oxygen, roads are gritted for free, and the whole thing earns the country billions every year — forever. That's CFF.

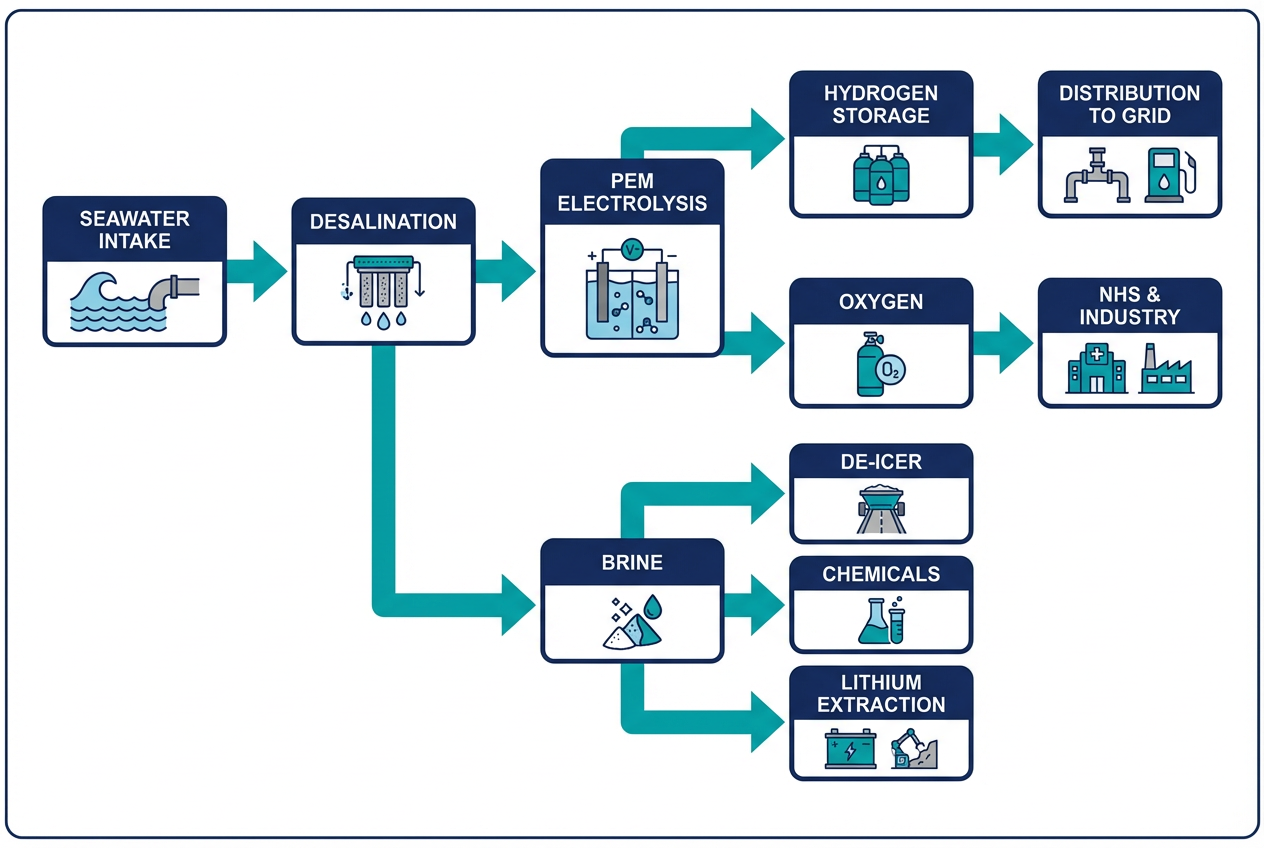

Carbon Free Future (CFF) is a plan to build 28 clean energy mega-sites around the UK's coastline — in England, Scotland, Wales, and Northern Ireland. Each site uses small, modern nuclear reactors to generate electricity, which then splits seawater into green hydrogen — a clean fuel that replaces natural gas.

But here's what makes this different from any other energy plan: nothing is wasted. Every single byproduct — heat, oxygen, salt, even lithium — becomes something valuable that benefits ordinary people directly.

The entire system is state-owned, meaning the profits go back to the nation, not to foreign shareholders. And because nuclear fuel lasts decades and the sites are designed for rolling maintenance, this infrastructure powers the UK not for 20 or 50 years — but for hundreds of years. The upfront cost becomes the biggest bargain in British history.

1.Build Clean Power Stations on the Coast

We place small, safe nuclear reactors (called SMRs) at 28 coastal sites across the UK — in England, Scotland, Wales, and Northern Ireland. They run on a tiny amount of fuel, produce zero carbon emissions, and generate enormous amounts of electricity — enough to power the entire country.

2.Turn Seawater into Green Hydrogen

That electricity splits seawater into hydrogen (a clean fuel) and oxygen. The hydrogen replaces natural gas — heating our homes, fuelling lorries, and powering factories — all without burning fossil fuels.

3.Free Heating for Nearby Communities

The reactors produce waste heat as a byproduct. Instead of throwing it away, we pipe it to every home within 10 miles — giving families completely free heating and hot water, saving around £2,000 a year.

4.Free Oxygen for the NHS

When we split water to make hydrogen, we also produce medical-grade oxygen — 28,000 tonnes per day. That's enough to supply every NHS hospital in the country, completely free of charge.

5.Free Advanced Road De-Icer for Councils

The desalination process produces brine as a byproduct. Rather than waste it, we produce advanced liquid brine road de-icer — enough to keep every road in the UK safe each winter, at no cost to local councils.

6.Energy Independence — No More Foreign Gas

Right now, the UK spends £50 billion a year importing oil and gas from unstable regions. CFF ends that dependency completely. We produce all our own energy, on our own soil, forever.

7.100,000+ UK Jobs

Workers from the North Sea oil and gas industry already have 80% of the skills needed. CFF's "Skills Passport" retrains and transitions them into well-paid, long-term clean energy careers — no one is left behind.

8.Pays for Itself — Then Earns £15–20 Billion a Year

The entire programme costs around £225 billion over 25 years. It pays for itself within 10–13 years through fuel savings and revenue. After that, it generates £15–20 billion per year for the nation — for the next 100+ years. That's over £1.5 trillion in total value, all state-owned.

Every UK Citizen Benefits

Whether you live next to a CFF site and receive free heating, drive on de-iced roads in winter, rely on the NHS for oxygen, fill up a hydrogen car, or simply benefit from a nation that no longer sends £50 billion abroad for gas — this project is for everyone.

Because CFF is 100% state-owned, every home and business gets their energy at cost + 5% — making the UK the cheapest place to live and do business in Europe. No shareholders to pay, no foreign profits to export. Just clean, affordable British energy for everyone.

Pay Once, Benefit Forever

Carbon Free Future represents the UK's most ambitious clean energy infrastructure programme—a 28-site national network across all four nations that transforms the United Kingdom from an energy importer into a self-sufficient Energy Superpower.

“For £225 billion—less than the UK spends on fossil fuel imports over 15 years—the nation gains permanent energy independence. Unlike oil wells that deplete, this infrastructure operates indefinitely: SMRs can be refurbished within the same facilities, hydrogen pipelines last centuries, and the knowledge developed becomes a permanent national asset.”

The Pathfinder Programme

First 6 sites (2025–2033) across England, Scotland, Wales, and Northern Ireland — each starting with a single SMR. Modular expansion as units roll off the factory floor.

Scale-Up Phase

Sites 7–17 (2033–2042) build on proven technology with parallel construction and 47% cost reduction through learning effects.

Full Independence

Sites 18–28 (2042–2055) complete the network. 92.1 GW baseload exceeds UK peak demand by 32 GW—the "Battery of Europe."

10–13 Year Payback

£225bn CAPEX pays for itself in a decade through eliminated fossil imports, then delivers £15–20bn/year in retained national wealth for 90+ years.

The Strategic Calculus

While other nations remain tethered to volatile global energy markets and the geopolitical whims of hydrocarbon exporters, the United Kingdom stands alone as a net energy exporter—the “Battery of Europe”—earning revenue from the same interconnectors that once drained national wealth. The £15–20 billion currently flowing annually to foreign oil and gas producers instead circulates within the domestic economy.

Standing on the Shoulders of Giants

The UK has always led the world in transformative infrastructure. CFF continues a 200-year tradition of nation-building mega-projects.

“The UK has delivered transformational infrastructure before—and can do so again. CFF's design incorporates lessons from 150 years of mega-project experience.”

🏛️ The UK's Infrastructure Legacy

Victorian Railway Boom

Created the world's first mass transport revolution. Connected every major town and industrial centre.

Lesson: The UK can deliver transformative national networks

National Grid

4,000 miles of 132kV transmission lines built in just 5 years. Unified Britain's electricity system.

Lesson: Centralized coordination delivers on time and budget

Railway Nationalization

Created British Railways from 4 private companies. Unified standards and coordinated services.

Lesson: National coordination enables system-wide optimization

Town Gas to Natural Gas

The most successful energy transition in British history. Centrally coordinated, free to consumers.

Lesson: Rapid national energy transitions are achievable

Motorway Network

Transformed the UK's road network and connected major cities with high-speed routes.

Lesson: Large-scale civil engineering is achievable at pace

Telecommunications

From analogue exchanges to fiber optic; the UK led in telecoms infrastructure rollout.

Lesson: Technology adoption at national scale creates lasting advantage

The Pathfinder Programme

Six strategically chosen coastal sites across the UK — each beginning with a single SMR and scaled desalination/PEM unit. The system is completely modular: additional units are added as they roll off the factory floor, proving the technology at minimal initial commitment before scaling to full capacity.

Modular Build Strategy

Each Pathfinder site starts with 1 SMR (470 MWe) plus proportionally scaled desalination and PEM electrolysis. This proves the integrated system at each location with minimal upfront cost. As factory-built SMR modules become available, each site grows towards its full 7-SMR capacity — a “crawl, walk, run” approach that de-risks the entire programme.

Pathfinder North

Teesside / Humber Region

Steel, Chemicals, HGV freight

Pathfinder Scotland

Grangemouth / Aberdeen Region

Distilling, North Sea transition, shipping

Pathfinder West

Milford Haven / Port Talbot

Glass manufacturing, Steel, Irish Sea logistics

Pathfinder South

Solent / Thames Estuary

Port decarbonisation, South-Coast grid stability

Pathfinder East

The Wash / East Anglia

Agriculture, food logistics, offshore wind backup

Pathfinder NI

Belfast Lough / Larne Coast

Agri-food processing, cross-border energy bridge, pharmaceuticals

Pathfinder Initial Capacity (1 SMR per site)

Each site then expands modularly towards full 7-SMR capacity as modules roll off the production line

Three Phases to Energy Independence

Phase 1: Pathfinder

Each site starts with 1 SMR — proving the modular system across all 6 UK zones. Additional SMRs added as they roll off the factory floor.

Phase 2: Scale-Up

New sites begin while Pathfinder sites expand to full capacity. Parallel builds (2–3 simultaneously), 47% cost reduction through learning effects.

Phase 3: Completion

Industrial production mode, mature cost floor, all 28 sites at full 7-SMR capacity. Full UK energy independence achieved.

| Year | Sites | Total SMRs | H₂ (t/day) | Grid (GW) | Phase |

|---|---|---|---|---|---|

| 2027 | 2 | 2 | 400 | 0.9 | Pathfinder |

| 2030 | 6 | 6 | 1,200 | 2.8 | Pathfinder |

| 2033 | 6 | 18 | 3,600 | 8.5 | Pathfinder ✓ |

| 2036 | 12 | 54 | 10,800 | 25.4 | Scale-Up |

| 2039 | 17 | 89 | 17,800 | 41.8 | Scale-Up |

| 2042 | 17 | 119 | 23,800 | 55.9 | Scale-Up ✓ |

| 2046 | 22 | 154 | 30,800 | 72.4 | Completion |

| 2050 | 26 | 182 | 36,400 | 85.6 | Completion |

| 2055 | 28 | 196 | 39,200 | 92.1 | COMPLETE ✓ |

Total Energy Independence

With 28 sites operational across all four UK nations, the United Kingdom achieves approximately 95% energy independence—eliminating vulnerability to global price shocks.

Power Generation

Exceeds UK peak demand by 32 GW—"Battery of Europe" export capability.

Hydrogen Production

Replaces all commercial transport fuel, industrial feedstock, and heating hydrogen.

Circular Economy

Lithium extraction, advanced road de-icer brine, NHS oxygen—every byproduct becomes revenue.

Economic Sovereignty

Fossil fuel import costs redirected to NHS, schools, and domestic prosperity.

UK Energy Independence Scorecard (2055)

Geopolitical Resilience

Critical Advantage: SMR fuel can be stockpiled for 2+ years in a warehouse-sized facility, providing unprecedented energy security against global supply disruptions.

The Best Infrastructure Investment in British History

£225 billion that pays for itself in 10–13 years, then delivers £15–20bn annually for 90+ years.

100-Year Value Creation

The “Quadruple Dividend” Economics

Energy Dividend

Selling energy at "Cost + 5%" once debt is serviced.

Industrial Dividend

Revenue from surplus by-products only — oxygen to steel/glass (after NHS served), brine feedstock (after winter de-icer obligation met), and lithium extraction.

Treasury Dividend

Billions saved via free oxygen to NHS, free de-icer to councils, plus billions in tax from a high-wage domestic workforce.

Water Dividend

Avoided costs from drought damage, crop failures and water trucking in dry years.

100% UK-Funded — Zero Foreign Investment

£225 billion funded entirely by the British public, for the British public. No foreign shareholders, no private equity taking profits offshore, no sovereign wealth fund from another country owning UK critical infrastructure.

The Core Principle

The UK already spends £50–60 billion per year on fossil fuel imports — gas, oil, and refined products. CFF does not create new spending. It redirects existing spending from foreign suppliers to domestic infrastructure. The government is not asking taxpayers for new money — it is asking them to invest in ending the payments they are already making.

Five Sovereign Funding Streams

CFF Infrastructure Bonds

£90–100bnLong-dated sovereign bonds (30–50 year gilts) issued specifically for CFF. Ring-fenced repayment from energy revenue — bondholders know exactly what their money builds and where repayment comes from. Issued in tranches aligned to each construction phase: ~£3–4bn/year during Pathfinder, scaling to £8–10bn/year during the main build.

UK Public Pension Fund Allocation

£60–70bnThe LGPS alone manages over £400bn. A 15–17% allocation across UK public-sector pension schemes (LGPS, NHS, Teachers', Civil Service) absorbs £60–70bn over 20 years. Infrastructure-backed, sovereign-guaranteed, inflation-linked sterling assets — exactly what pension trustees need. Every penny stays within the UK public sector.

People's Energy Bonds (NS&I)

£25–30bnA new NS&I savings product at 4.0–4.5% tax-free — better than Premium Bonds and backed by real energy infrastructure. Gives ordinary citizens a direct stake in UK energy independence. Even a modest 10–15% of NS&I capacity over the build period delivers £25–30bn.

Fossil Fuel Import Savings Recycling

£15–20bn/yr from ~2038The self-funding engine. Once 10–12 sites are operational (~2038–2040), the UK's fossil fuel import bill falls dramatically. Those savings — £15–20bn/year — are hypothecated directly back into CFF construction. By Phase 3, the project pays for its own completion from money no longer sent to Qatar, Norway, and Saudi Arabia.

Bank of England Green Infrastructure Facility

£20–30bnA dedicated facility lending to HM Treasury at base rate for CFF construction — low-cost bridging finance before revenue kicks in. Not money-printing; the central bank lending to its own government for productive capital investment that directly reduces inflation risk by eliminating volatile fossil fuel import costs.

The Self-Funding Arithmetic

Crossover point — where annual savings exceed annual build costs — arrives around 2039–2041. From that point, CFF is a net contributor to the Exchequer.

| Period | Annual Spend | Revenue / Savings | Net Position |

|---|---|---|---|

| 2025–2033Pathfinder | ~£4bn/yr | Minimal — proving phase | –£4bn/yrFunded by bonds |

| 2033–2040Scale-Up | ~£8–10bn/yr | £5–10bn/yr savings begin | –£3–5bn/yrGap narrowing |

| 2040–2048Acceleration | ~£8bn/yr | £15–20bn/yr savings | +£7–12bn/yrSurplus begins |

| 2048–2055Completion | ~£4bn/yr | £20bn+/yr + H₂ exports | +£16bn+/yrStrong surplus |

| 2055+Operational | ~£2bn/yr maintenance | £20–25bn/yr revenue | +£18–23bn/yrPerpetual return |

The Social Contract — Free By-Products

CFF by-products serve the public first. Heat, oxygen, and de-icer are provided free of charge to communities within 10 miles, every NHS facility, and every council in the UK. Revenue comes only from surplus sold commercially.

Free Oxygen — NHS & Councils First

All 28 sites produce 28,000 tonnes/day of medical-grade oxygen. Every NHS hospital and local council in the UK receives oxygen at zero cost — no exceptions. Only after NHS and council demand is fully met is surplus oxygen sold to industrial users such as steel and glass manufacturers.

Free De-Icer — Communities & Councils First

Advanced road de-icer from concentrated brine is provided free to every council and every community within 10 miles of a CFF site. In spring, summer, and autumn — when de-icer is not required — surplus brine is sold as chemical feedstock to generate revenue. Winter supply to councils and communities is always free.

Surplus Sales — Revenue After Obligation

Revenue comes only from surplus by-products sold commercially after all free obligations are met. Oxygen to industrial agents (steel, glass, chemicals) and brine as chemical feedstock during warmer months. The free provision is a social contract — the revenue is a bonus, never a priority over public service.

Revenue Streams That Repay Bondholders

The Chancellor's Pitch

“We are not borrowing to spend. We are investing to save. Every pound in a CFF bond replaces a pound we currently send overseas for gas and oil. Within 15 years, this investment pays for itself. Within 30 years, it delivers permanent energy sovereignty and a £20 billion annual surplus — owned entirely by the British public, funded entirely by the British public.”

No foreign shareholders. No private equity taking profits offshore. No sovereign wealth fund from another country owning UK critical infrastructure. The pensions of British workers funding the energy security of British workers.

The Cheapest Energy in the Developed World

Once the UK owns its energy system outright, the only costs are operational — no shareholders, no foreign fuel imports, no carbon levies. Here is what that means for every household and driver in the country.

The Pricing Principle — "Cost + 5%"

After the 10–13 year payback period, CFF infrastructure is fully owned by the state — debt-free. At that point, energy is sold at production cost plus a 5% reinvestment margin. No profit extraction, no dividends to foreign investors, no volatile global commodity pricing. The 5% margin funds ongoing maintenance, upgrades, and the national energy reserve. Every penny of savings stays in the pockets of UK households and businesses.

Electricity

Nuclear marginal cost is £20–25/MWh worldwide. SMR mass-production drives it lower. Add grid distribution and a 5% reinvestment margin — still under 7p/kWh. No gas import cost, no carbon levy, no shareholder dividend.

Home Heating (H₂ Boiler)

Hydrogen produced at £1.50–2.00/kg from nuclear electrolysis with no fuel import cost and paid-off electrolysers. Hydrogen boilers use existing gas pipework — no expensive heat pump retrofits needed. Free district heating within 10 miles of each site eliminates heating bills entirely for millions.

Vehicle Fuel (H₂ at pump)

Hydrogen fuel cell vehicles achieve ~60 miles per kg. At £3.50–4.50/kg pump price (production cost + compression + distribution), that is 6–7.5p per mile — cheaper than petrol at 8p per mile. Zero emissions, 3-minute refuelling, and far lower maintenance costs than internal combustion engines.

International Comparison

How CFF pricing stacks up against nations with the cheapest energy in the developed world.

| Country | Electricity /kWh | Gas/H₂ /kWh | Fuel |

|---|---|---|---|

| 🇬🇧UK Today | 24.5p | 7.0p | 145p/L |

| 🇫🇷France (nuclear) | ~20p | ~7p | ~155p/L |

| 🇳🇴Norway (hydro) | ~8–12p | N/A | ~165p/L |

| 🇺🇸USA average | ~13p | ~4p | ~90p/L |

| 🇬🇧CFF UK (projected) | 5–7p | 3–4.5p | 6–7.5p/mi |

Millions Pay Nothing at All

Remember — every home and business within 10 miles of a CFF site receives free district heating from SMR waste heat. With 28 sites across the UK, that covers millions of households whose heating bill drops to zero. Add free oxygen to NHS hospitals, free de-icer to councils, and free fresh water from desalination — and CFF is not just cheap energy, it is a complete public service.

Pricing Methodology & Disclaimer

These projections are based on known nuclear marginal operating costs (£20–25/MWh globally), current green hydrogen production benchmarks, and the principle that state-owned infrastructure operates at "Cost + 5%" with no shareholder profit extraction once capital debt is retired. Current UK prices sourced from Ofgem price cap data (2024/25). International comparisons use IEA and Eurostat published averages. Actual prices will depend on final build costs, operational efficiency, and government pricing policy. All figures are illustrative projections for a state-owned energy system — not commercial forecasts.

Access CFF Materials

Download documentation, listen to our podcast, and explore the complete CFF technical library.

Documentation Pack

Download the complete CFF documentation including technical specifications, financial models, rollout timelines, and supporting research materials.

CFF Podcast

Listen to an in-depth discussion exploring the Carbon Free Future initiative, its technical foundations, and the pathway to UK energy sovereignty.

Listen to the CFF Podcast

Technical Documents

CFF UK National Vision 2055

Combined national vision document outlining the complete CFF programme.

2055 Blueprint (Master v4)

The definitive blueprint covering all technical, financial and operational aspects.

10-Mile Heat Halo Policy

Policy document for free district heating within 10 miles of each CFF site.

Swiss Army Knife Infographic

Visual summary of CFF's multi-purpose capabilities—the grid Swiss Army Knife.

Blueprint Book v2

Earlier comprehensive version of the CFF blueprint documentation.

Blueprint Book v5

Latest version of the CFF blueprint book with updated projections.

Sea-to-Street: The Complete Hydrogen Chain

From seawater intake to hydrogen-powered HGVs on British roads — a fully integrated clean energy system.

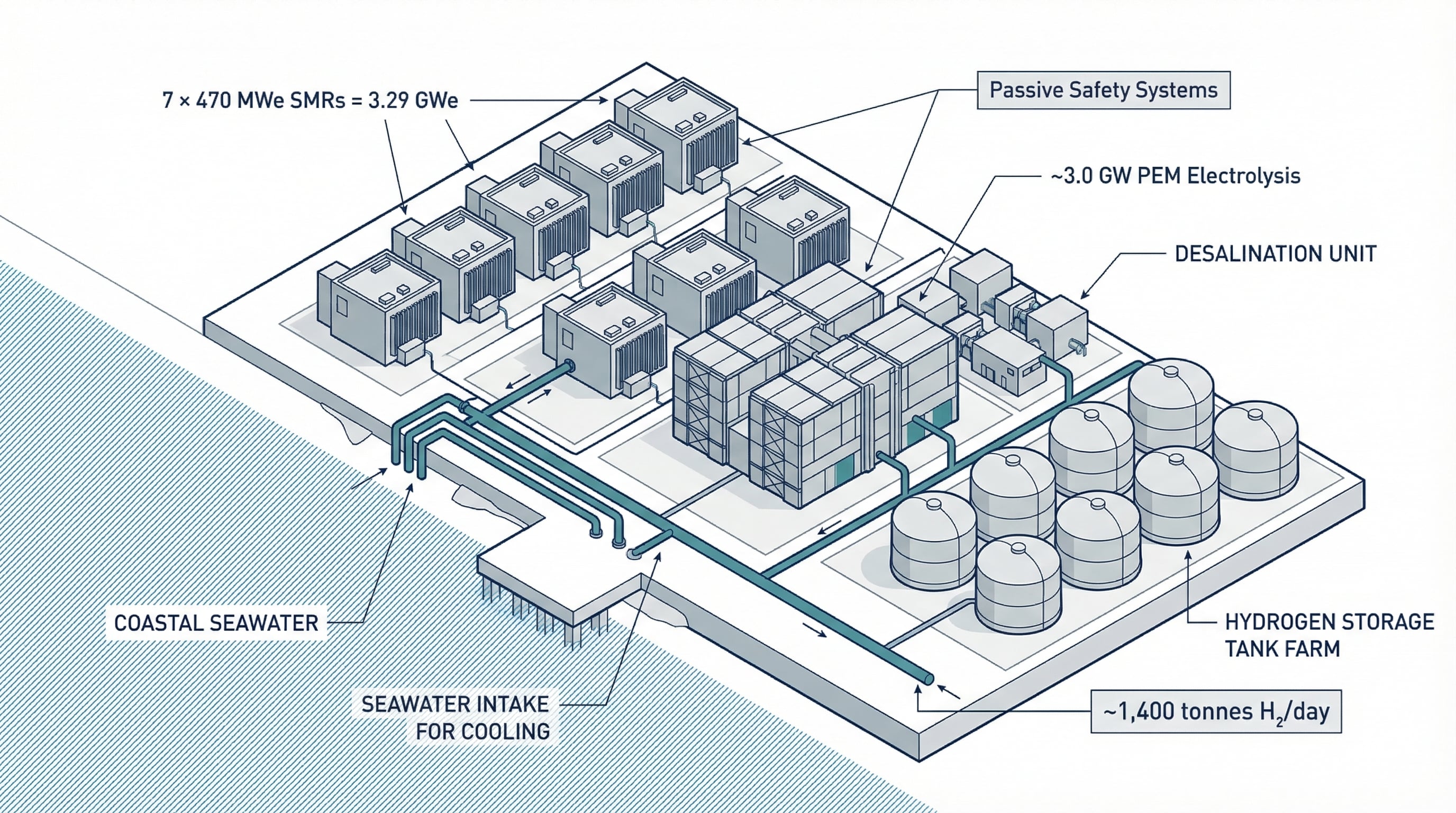

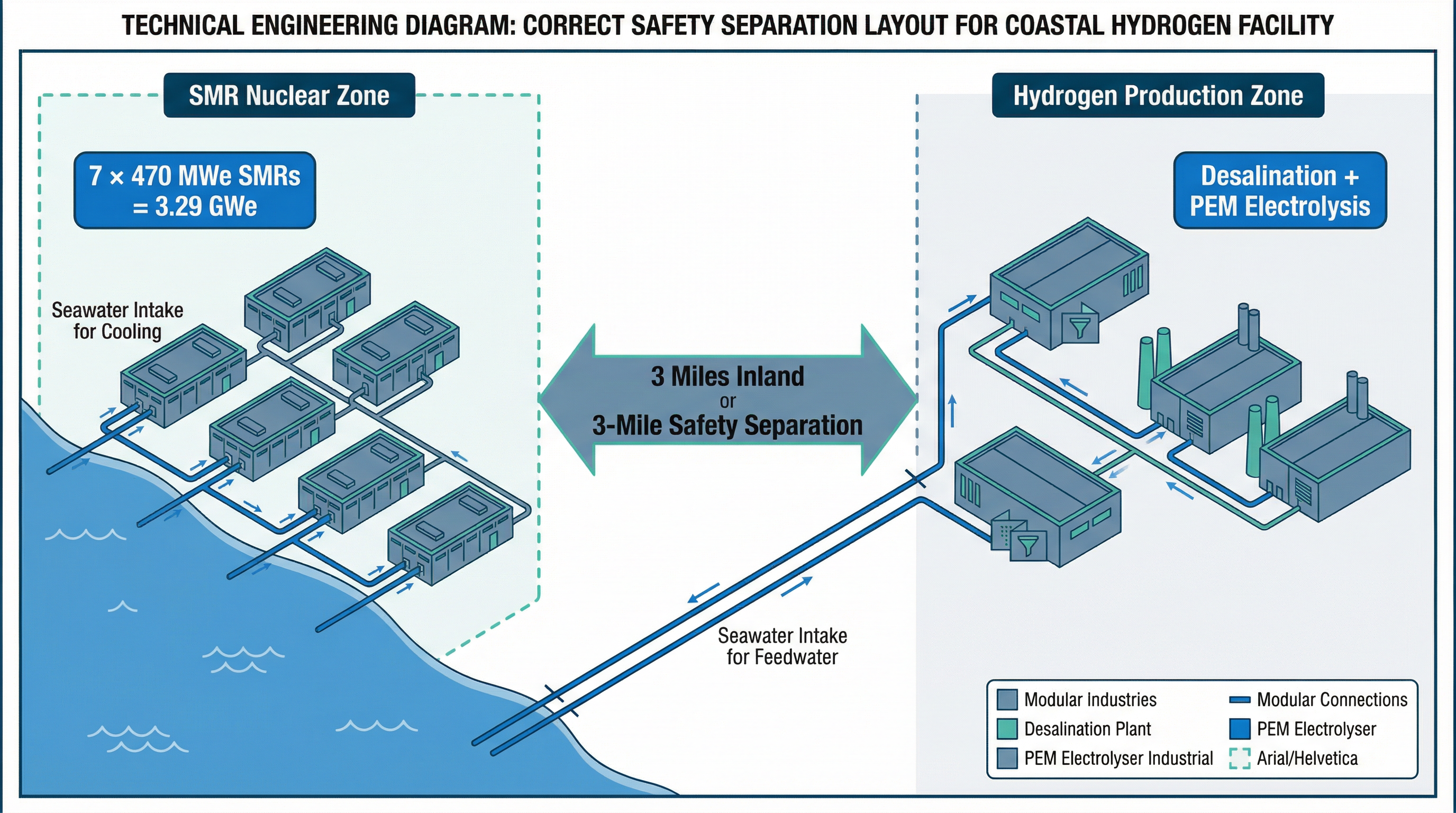

1. Coastal Power Hub

Onshore coastal facilities house 7 SMR units per site, producing constant baseload electricity. Power is transmitted overland to hydrogen production zones located 3 miles inland.

2. Desalination & Electrolysis

Located 3 miles from SMR facilities. Seawater intake pipes supply feedwater for desalination before entering PEM electrolysers that split water into hydrogen and medical-grade oxygen.

3. Pipeline Export

Compressed hydrogen flows through onshore pipelines to industrial terminals at Teesside, Humber, and other regional hubs.

4. Industrial Decarbonisation

Major industrial users receive hydrogen directly, replacing fossil fuels in chemicals, refining, steelmaking, and high-temperature manufacturing.

5. Refuelling Infrastructure

Hydrogen distribution extends to refuelling hubs serving HGVs, buses, and locomotives with rapid 15-minute fills comparable to diesel.

6. Clean Mobility

Fuel cell HGVs convert hydrogen to electricity via electrochemical reaction, producing only water vapour at the tailpipe while maintaining full payload capacity.

Per-Site Technical Architecture

Each CFF Mega-Site is a fully integrated onshore coastal energy production facility.

Hybrid-Ready Design

The system allows dynamic switching between hydrogen production and grid electricity injection, acting as a national “Safety Valve” during periods of low renewable output.

| Metric | Pathfinder Initial (6 × 1 SMR) | Full Scale (28 Sites) |

|---|---|---|

| Total SMRs | 6 | 196 |

| Total Capacity | 2.8 GW | 92.1 GW |

| H₂ Production | 1,200 t/day | 39,200 t/day |

| PEM Capacity | ~2.5 GW | ~81.2 GW |

| UK Demand Coverage | ~5% | 154% |

3-Mile Safety Separation Zone

A critical safety requirement ensuring physical separation between nuclear and hydrogen production facilities.

Onshore Coastal Facility Design

Both zones are located onshore at coastal sites. The SMR zone is positioned closer to the shoreline for seawater cooling access, while the desalination/PEM zone is located 3 miles inland for safety.

Nuclear Safety Compliance

Meets regulatory requirements for emergency planning zones around nuclear facilities.

Hydrogen Hazard Isolation

Separates hydrogen production and storage from the nuclear plant to prevent cascading risks.

Power Transmission

Overland cables safely transmit electricity from the coastal SMR zone to the inland H₂ production facility.

Seawater Access

Intake pipework extends into the sea for SMR cooling water and desalination feedwater — the only offshore element.

Onshore Zone Architecture

SMR Zone (Coastal): 7 × 470 MWe reactors with control facilities; seawater intake pipes for cooling.

H₂ Production Zone (3 miles inland): Desalination plant, PEM electrolysers, hydrogen compression, and pipeline export infrastructure.

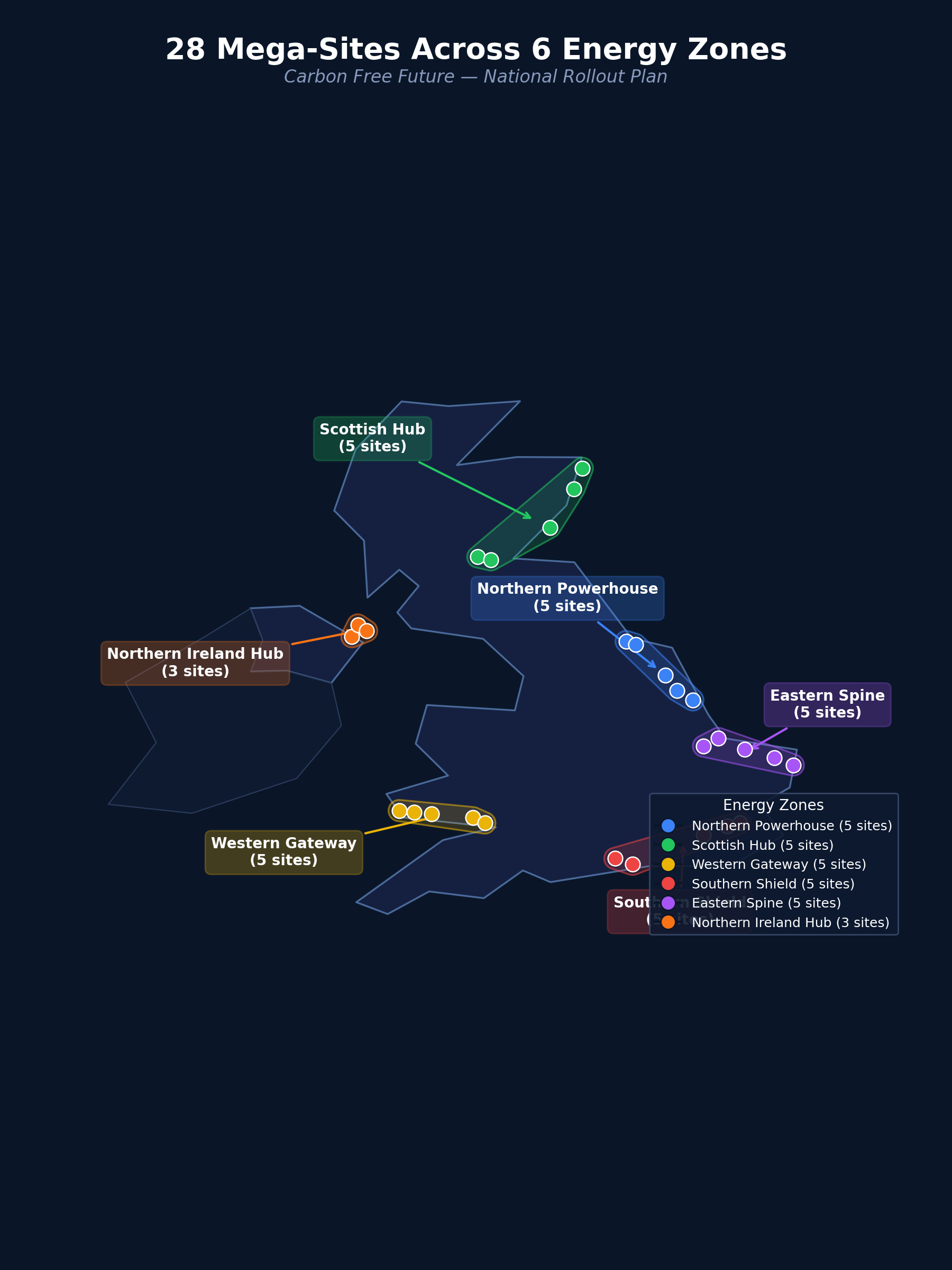

28 Mega-Sites Across 6 Energy Zones

Strategic distribution ensures resilience, redundancy, and regional economic benefits across the entire United Kingdom — from Scotland to Southern England, Wales to Northern Ireland.

Northern Powerhouse

5 Mega-Sites • Teesside/Humber Region

Primary: Steel, Chemicals, North-South HGV freight

Scottish Hub

5 Mega-Sites • Grangemouth/Aberdeen Region

Primary: Distilling, North Sea transition, heavy shipping

Western Gateway

5 Mega-Sites • Milford Haven/Port Talbot Region

Primary: Glass manufacturing, Steel, Irish Sea logistics

Southern Shield

5 Mega-Sites • Solent/Thames Estuary Region

Primary: Port decarbonisation, South-Coast grid stability

Eastern Spine

5 Mega-Sites • The Wash/East Anglia Region

Primary: Agriculture, food logistics, offshore wind backup

Northern Ireland Hub

3 Mega-Sites • Belfast Lough/Larne Coast Region

Primary: Agri-food processing, cross-border energy bridge, pharmaceuticals

Complete Circular Economy

Every output serves the public first — free oxygen to NHS, free de-icer to councils — with only surplus sold commercially.

Oxygen — NHS & Councils First

Free to NHS & CouncilsHigh-grade O₂ produced during electrolysis (8 kg for every 1 kg H₂). 28 sites = 28,000 tonnes/day oxygen — provided free to every NHS facility and every council in the UK. Only surplus oxygen, after all public needs are met, is sold to industrial users such as steel and glass manufacturers.

Brine — Communities & Councils First

Free De-Icer in WinterRO brine concentrated using PEM waste heat, producing 21M litres/day of premium road de-icer with enhanced magnesium content — free to every council and every community within 10 miles. Surplus brine sold as chemical feedstock in spring, summer, and autumn when de-icer is not required.

Lithium Extraction

Critical MineralsDirect Lithium Extraction (DLE) from concentrated brine provides domestic battery-grade lithium supply, reducing China dependence.

Water Cycle Closure

Strategic Water ReserveH₂ combustion returns water vapour to the natural cycle — the same closed-loop system nature uses. Sea water becomes fuel becomes water.

Decarbonising Hard-to-Abate Sectors

The final 30–40% of UK emissions that electricity alone cannot address — solved with 39,200 tonnes of hydrogen per day from 28 sites.

Steel Manufacturing

Hydrogen replaces coking coal in high-temperature reduction processes, enabling "Green Steel" production.

Chemicals & Refining

High-purity hydrogen as feedstock decouples chemical plants from volatile gas markets.

Glass Production

High-temperature furnaces powered by hydrogen combustion deliver intense heat for glass manufacturing.

Cement & Ceramics

Industrial kilns transition from natural gas to hydrogen, maintaining essential temperatures.

HGV Logistics

Fuel cell HGVs: same range, 15-minute refuelling, full payload. 15,000 t/day H₂ for all 500,000 UK HGVs.

Domestic Heating

70% of homes use H₂ boilers (existing stock), 30% heat pumps (new builds). 8,000 t/day H₂ replaces gas heating.

10-Mile Heat Halo & Grid Impact

Free district heating within 10 miles of each site, plus keeping the grid stable without £100bn+ upgrades.

The Problem: All-Electric Future

In a battery-led future with 100% heat pumps, the UK grid must deliver 187 GW at peak — requiring 3× today's infrastructure capacity. Every car charging overnight, every heat pump on cold mornings creates massive demand spikes.

The Solution: CFF Mixed Approach

With 30% heat pumps and 70% hydrogen boilers, plus hydrogen vehicles that don't plug in, peak demand drops to just 65 GW — fitting within today's grid infrastructure.

10-Mile Heat Halo

Each CFF site produces enormous amounts of waste heat from SMR operations. Rather than dumping it, this heat is distributed as free district heating to all homes and businesses within a 10-mile radius.

The “Impossible Trilemma” — Solved

Without hydrogen, the UK faces an unpalatable choice: rebuild the entire electricity grid at £100+ billion cost to handle battery EV charging (187 GW peak demand), or fail to decarbonise heavy transport and industry entirely. CFF's hybrid approach uses hydrogen as an energy carrier for transport and heat while providing baseload grid power.

“Safe-Flex” Grid Support

CFF sites keep reactors at 100% output and flex electrolysers as a controllable load — giving the grid ~40 GW of emergency power.

How Safe-Flex Works

In normal operation, most SMR output (~2.3–2.9 GW per site) runs electrolysers to produce hydrogen.

When the grid is under stress (cold, still winter evening), electrolysers are ramped down towards a 50% floor.

Freed-up power is diverted to the grid — up to ~40 GW across the fleet, equivalent to UK peak demand on a typical winter day.

Even in maximum grid-support mode: hydrogen continues at ~50%, oxygen and brine flows continue, hospitals and councils still receive free supplies.

National Water Security

Each site includes a dedicated “Unit 8” Desalination Train solely for national water security.

Each site's dedicated water unit

Enough for 9–11 million people

~10 MW from 3,300 MW site output

Agricultural Spine pipeline system

Water-for-Food Security

In a dry spring, Unit 8 is activated, pumping water into a dedicated “Agricultural Spine” pipeline. This ensures that even in a severe drought, the UK's vegetable and grain belts never fail — effectively de-coupling food production from rainfall.

Ultra-Pure Water for Agriculture

PEM electrolysers require ultra-pure water — cleaner than typical drinking water. Once re-mineralised, it is ideal for vertical farms and greenhouses co-located at CFF sites, using waste heat from SMRs for high-value crops.

Skills Passport: North Sea to Hydrogen

80% skills overlap enables seamless workforce transition from oil & gas to clean energy across all 28 sites.

Safety Systems Expertise

BOSIET/HUET and industrial safety certifications transfer directly to coastal hydrogen facility operations

High-Pressure Gas Handling

Pipeline and compression expertise applies to H₂ systems

Electrical & Instrumentation

Control systems knowledge transfers to PEM electrolysers

Mechanical Engineering

Maintenance skills apply to SMR and desalination systems

Process Operations

Production control experience valuable for hydrogen operations

Nuclear Upskilling

Additional certification for SMR-specific operations provided

Protecting Communities

CFF sites are deliberately co-located with existing O&G infrastructure. The Skills Passport ensures the energy transition creates jobs in the same communities where fossil fuel jobs are being phased out — a true “just transition.”

The UK as an Energy Superpower

Partner with Carbon Free Future

Join the UK's most ambitious clean energy infrastructure programme — from Pathfinder to Energy Superpower.

Government & Policy

Shape the regulatory framework that enables energy sovereignty. Support planning, permitting, and national infrastructure designation.

Industry Partners

Secure long-term hydrogen supply agreements. First-mover advantage for hard-to-abate sector decarbonisation.

Investors

Infrastructure-grade returns with sovereign backing. 10–13 year payback, then £15–20bn/year retained nationally for 90+ years.